Deliberating on IFRS Sustainability Disclosure Standards: Future incorporation of Double Materiality principle for sustainability impact assessment

In 2024, WT began studying the IFRS Sustainability Disclosure Standards and plans to incorporate the Double Materiality principle (including Impact Materiality and Financial Materiality) as the method for sustainability impact assessment in the future. By comprehensively considering sustainability reporting standards (GRI, SASB), international sustainability ratings (MSCI, S&P CSA, CDP), benchmarking of industry best practices, and other factors, we collected relevant sustainability topics. We also evaluated issues of concern to five key stakeholder groups, analyzing potential impacts from business operations and value chain relationships. Through this process, we identified a list of 19 material sustainability topics. In 2022, WT conducted a sustainability topic questionnaire survey to understand key stakeholders’ concerns and expectations regarding WT’s sustainability management, receiving 611 valid responses. In 2024, after reassessing changes in the operating environment, the Sustainability Task Force determined that sustainability impacts remained largely unchanged from 2023. Therefore, we maintained the same sustainability topics as 2023, which serve as the basis for disclosures in this Sustainability Report.

Relevant GRI material topics of the top three issues

The survey results were analyzed to find out the top three sustainability issues of concern for each stakeholder group. WT matched the issues to GRI material topics, and disclosed relevant implementation strategies, managing policies and plans accordingly.

Stakeholder groups Top three issues of concern

Shareholders / BanksEthical Corporate ManagementEconomic impactTalent attraction and retentionCustomersInformation securityProduct responsibilitySustainable supply chainEmployeesEthical Corporate ManagementInformation securityTalent attraction and retentionVendorsSustainable supply chainInnovation managementProduct responsibilityOther SuppliersEthical Corporate ManagementHuman capital developmentSustainable supply chain

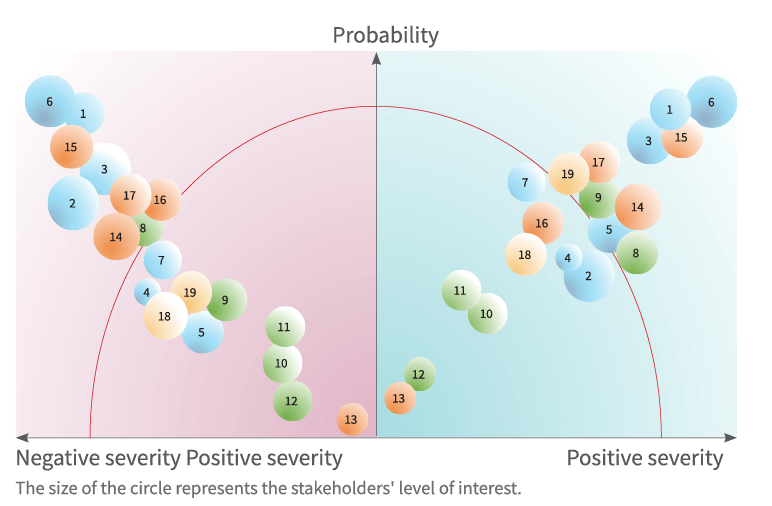

Impact Analysis Results by Sustainability Issues

Negative Positive 1 ● ● Economic impact 2 ● Ethical corporate management 3 ● ● Sustainable supply chain 4 Tax management 5 ● Innovation management 6 ● ● Information security 7 Quality management 8 ● ● Climate strategies 9 ● Energy management 10 Water resource management 11 Waste management 12 Air pollution management 13 Biodiversity 14 ● ● Product responsibility 15 ● ● Talent attraction and retention 16 ● ● Diversity, inclusion and equality 17 ● ● Human capital development 18 Occupational safety and health 19 ● Social impact Assessment of actual and potential impacts

The sustainability impacts were assessed for severity and probability by our Sustainable Development Team members. The severity is evaluated by the levels of positive and negative impacts. An issue involving an actual or potential human rights risk is assigned the highest severity level. With the stakeholders’ degrees of concern for the issues also taken into account, a three-dimensional analysis matrix was created as an impact level assessment tool to continuously track the impacts of the sustainability issues.

12 material issues disclosed in 2024 Sustainability Report

In 2024, WT’s Sustainable Development Team conducted a comprehensive assessment of the economic, environmental, and social operational impacts and their likelihood across the company’s business activities. Following this evaluation, the team decided to maintain the same 12 material issues identified in 2023 as the basis for disclosure in the 2024 Sustainability Report.

Description of material disclosure issues

15 GRI material topics plus 3 self-defined topics

We matched the selected disclosures with the 33 economical, environmental or social topics of the GRI Sustainability Reporting Standards, and identified 15 relevant material topics and the disclosure indicators related to these topics.

Organizational boundary definition for the Sustainability Report

The key disclosure issues were individually reviewed for their respective impacts on WT and throughout the value chain at Sustainable Development Team meetings, where the team members also determined that the organizational boundary of the Report and the definition of impact scope would vary slightly with different issues.

Sorted by positive impactSorted by negative impactInformation Security*01Information Security*Economic impact*02Talent attraction and retention*Talent attraction and retention*03Economic impact*Sustainable supply chain*04Sustainable supply chain*Human capital development*05Ethical corporate management*Product responsibility*06Product responsibility*Innovation management*07Human capital development*Climate strategies*08Climate strategies*Energy management*09Diversity, inclusion and equality*Social impact*10Quality managementSorted by positive impactSorted by negative impactQuality management11Occupational safety and healthDiversity, inclusion and equality12Tax managementEthical corporate management13Energy managementTax management14Social impactOccupational safety and health15Innovation managementWaste management16Waste managementWater resource management17Water resource managementAir pollution management18Air pollution managementBiodiversity19Biodiversity*Material impact issues

Note 2: Nature of impact: positive █ (beneficial to stakeholders) / negative ▲ (adverse to stakeholders)

Analysis of material disclose issues

The last report was released in Augest 2024. This report was released in Augest 2025. Contact:Sustainable Development Team Address:14F, No.738, Chung Cheng Road, Chung Ho District, New Taipei City 235603, Taiwan (R.O.C.) Telephone:+886-2-8226-9088 Email:esg@wtmec.com Privacy Policy

Copyright© WT Microelectronics Co., Ltd., All Rights Reserved.